Internal Controls for the Acquisition and Payment Cycle

Design tests of controls substantive tests of transactions Describe the methodology for designing tests for the details Conducting an Audit Plan Risks for the Audit of the Acquisition Audit objectives misstatements. Prenumbered receiving reports are prepared as support for acquisitions and numeri-.

Purchase And Payment Cycle

Managers often think of internal controls as the purview and responsibility of accountants and auditors.

. 13-26 Objectives 13-1 13-4 13-5 The following are independent internal controls commonly found in the acquisition and payment cycle. Purchase returns and allowances and purchase discounts. By KING SHU JUAN CEA150041 1.

Auditing and Internal Control. The following are independent internal controls commonly found in the acquisition and payment cycle. Understand internal control.

In this session I will discuss acquisition and payment cycleAre you a CPA candidate or accounting student. Acquisitions of goods and services 2. What are the four key internal controls for the acquisition and payment cycle.

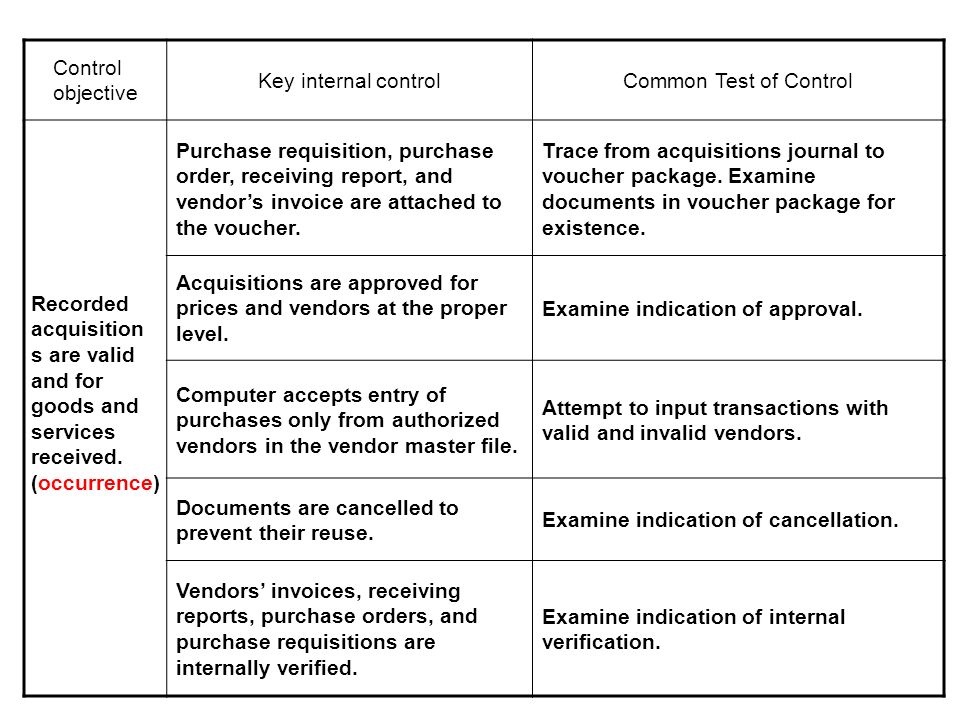

Tests of Controls Substantive Tests of Transactions and Accounts Payable. Implementing the Five Key Internal Controls Purpose Internal controls are processes put into place by management to help an organization operate efficiently and effectively to achieve its objectives. The following internal controls for the acquisition and payment cycle were selected from a standard internal control questionnaire1.

Purchase returns and allowances and discounts There are 10 accounts involved in the acquisition and payment cycle you can see it in. 221 Internal controls for purchase and payment cycle is mainly concerned about the following aspects. All supporting documents are cancelled after checks are signed or electronic funds transfers are approved.

Tests of controls and substantive tests of transactions for the acquisition and payment cycle are divided into 2 broad areas. The following internal controls for the acquisition and payment 1. The authorized signer.

Its easy for things to go wrong in a companys acquisition and payment cycle. Final assessment opportunity 2016. Acquisitions of goods and services 12.

Each control is to be considered independently. Before a check is prepared to pay for acquisitions by the accounts payable department the related purchase order and receiving report are attached to the vendors invoice being paid. Understand internal control and design and perform tests of controls and substantive tests of transactions for the acquisition and payment cycle.

Describe the business functions and the related documents and records in the acquisition and payment cycle. Types of Audit Tests for the Acquisition and Payment Cycle Accounts Payable Payments Expenses Audited by TOC STOT and AP Audited by TOC STOT and AP Ending balance Audited by AP and TDB TOC STOT AP TDB Cash in Bank Acquisition Expenses Ending balance Audited by AP Sufficient appropriate evidence per GAAS 2008 Prentice Hall. Each control is to be considered independently.

Tests of Controls Substantive Tests of Transactions and Accounts Payable. There are 3 classes of transactions included in the cycle. Prenumbered receiving reports are prepared as support for acquisitions and numeri-cally accounted for3.

Processing purchase orders receiving goods and services recognizing the liability. Approved purchase orders are required for all acquisitions of goods2. Transactions in the acquisition and payment cycle.

Companies can overstate the value of the inventory they purchase which makes assets look bigger than they actually are. Approved purchase orders are required for all acquisitions of goods. Control Procedures over Purchases and Payables As with the sales system there are a large number of controls that may be required in the purchases cycle due to the importance of this area in any business and once again the following list is classified by type of.

How to Audit the Acquisition Payment Cycle. Tests of acquisitions involve 3 of 4 business functions. The acquisition and payment cycle is a computerized process that is integrated with supply chain management is the management and control of materials in the logistics process from the acquisition of raw materials to the delivery of finished products to the end user.

Medium Discuss the key internal controls that should be present in the processing purchase orders function in the acquisitions and payment cycle. The following internal controls for the acquisition and payment cycle were selected from a standard internal control questionnaire. Acquisition and payment cycle Inventory and production cycle Finance cycle Investment cycle 10 20 20 15 20 15 18 minutes 36 minutes 36 minutes 27 minutes 36 minutes 27 minutes 100 180 minutes.

Answer of 1. Chapter 18 2012 Prentice Hall Business Publishing Auditing 14e ArensElderBeasley 18 - 2. Audit of the Acquisition and Payment Cycle.

Proper authorization both general and specific for acquisition transactions is an essential internal control of the processing purchase orders function. Disbursement payable cycle benefits of audit sampling Apollo Shoes Audit program design. Dates on receiving reports are compared.

A Proper authorization of purchases. Checks are mailed by the owner or manager or a person under her supervision after signing. Classes of transactions 11.

At the end of each month an accounting clerk accounts for all prenumbered receiving reports documents evidencing the receipt of goods issued during the month and traces each one to the related vendors invoice and acquisitions. Check my website for additional resources such. Briefly explain the procedures in place that would suggest these.

Management can omit or undervalue their accounts payable. The fact is that management at all. Understand Internal Control The auditor gains an understanding of internal control for the acquisition and payment cycle by studying the clients flowcharts preparing internal control questionnaires and performing walk-through.

Audit of the Acquisition and Payment Cycle.

Chapter 11 Audit Of Acquisition And Payment Cycle And Inventory Ppt Video Online Download

Audit Of The Acquisition And Payment Cycle Ppt Video Online Download

Chapter 18 Audit Of The Acquisition And Payment Cycle Ppt Video Online Download

Comments

Post a Comment